blog

Personal Loans for Those with Weak Credit: A Practical Guide for 2026

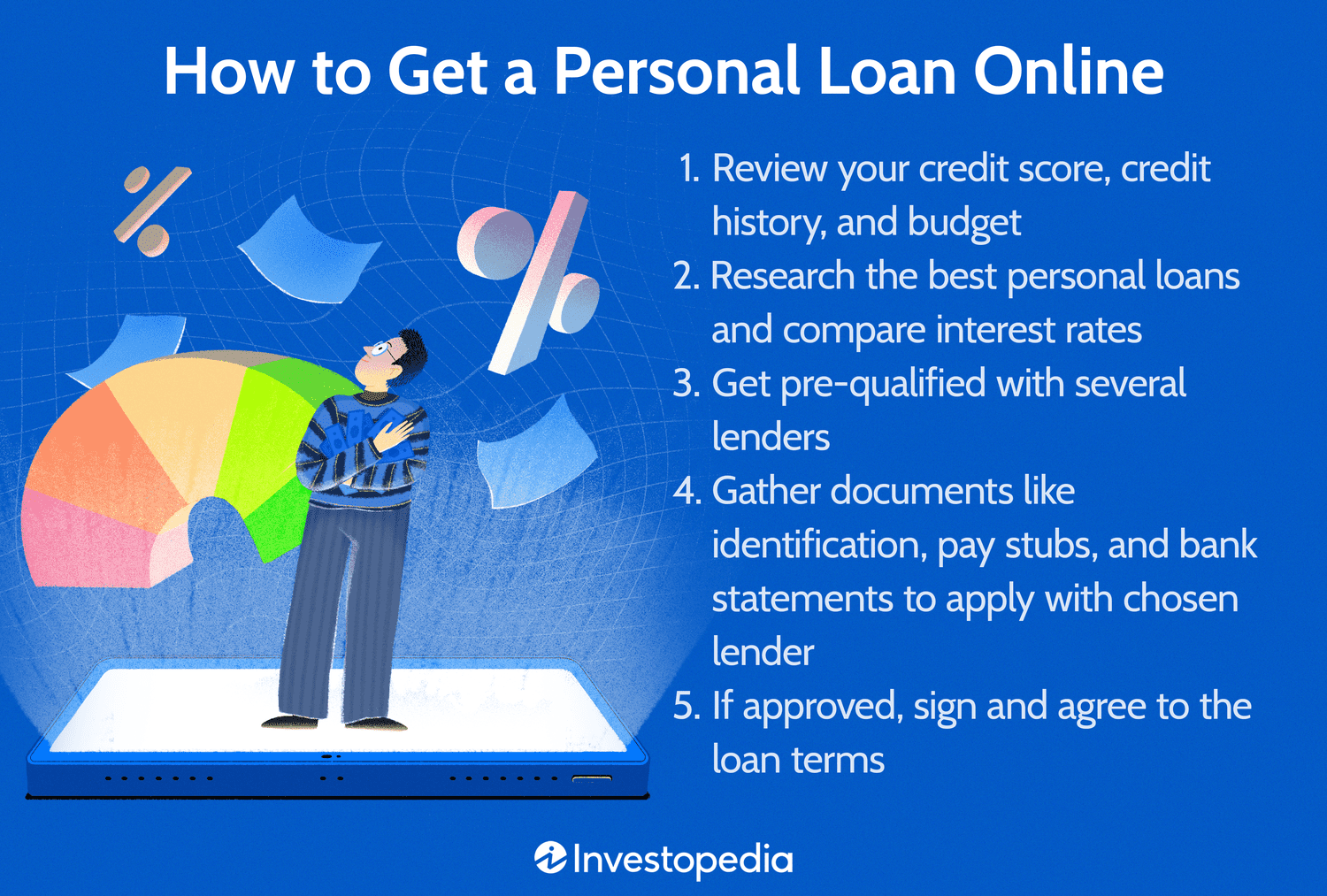

In the ever?shifting landscape of consumer finance, a growing number of borrowers find themselves navigating the maze of personal loan options after a dip in their credit scores. Whether you’re juggling unexpected expenses or planning a home improvement project, understanding the nuances of low?credit?score lending can make all the difference.

While the market offers an array of products—ranging from payday lenders to fintech platforms—only a handful combine affordability with transparent terms for those scoring below 580. The following article pulls together real?world data, expert insights, and recent regulatory changes to help you decide where to turn next.

Why Credit Scores Matter in Personal Lending

Credit scores are the industry’s shorthand for risk. Lenders use them to predict whether a borrower will repay on time. A score under 580 typically signals higher default risk, which in turn pushes lenders to charge steeper interest rates or demand collateral.

Yet it isn’t all doom and gloom. Many modern platforms have begun leveraging alternative data—such as employment history, education, and even payment patterns for utilities—to assess creditworthiness beyond the traditional FICO metric.

- FICO Score: The most widely recognised model, ranging from 300 to 850.

- Alternative Scores: Models like VantageScore or proprietary AI?driven algorithms that factor in non?credit data.

- Credit Utilisation Ratio: A lower ratio can offset a modest score, showing responsible borrowing habits.

Regulatory Safeguards for Low?Score Borrowers

The Consumer Financial Protection Bureau (CFPB) has tightened rules around high?cost loans, especially those targeting vulnerable consumers. Notably:

- Maximum APR Caps: In many states, the maximum annual percentage rate (APR) for unsecured personal loans is capped at 36%.

- Fee Transparency: Lenders must disclose all fees—origination, late payment, pre?payment—in plain language.

- No Pre?payment Penalties: Many lenders now waive penalties for early repayment to encourage debt reduction.

These changes aim to level the playing field, ensuring that borrowers with lower scores aren’t trapped in a cycle of expensive borrowing.

The Rise of AI?Driven Lenders: Upstart and Avant Take the Lead

AI?powered platforms have redefined how credit decisions are made. By analysing thousands of non?credit variables, they can spot patterns that traditional models miss. Two names dominate this space:

- Upstart: Uses education, employment, and income data to grant loans as low as £1,000 for borrowers with scores from 300 upwards.

- Avant: Offers unsecured personal loans up to £75,000, focusing on flexible repayment terms and no pre?payment fees.

Both platforms provide a quick online application process that can deliver approval decisions within minutes. However, the interest rates still reflect the borrower’s risk profile; those with lower scores will see rates in the 15–25% range.

Case Study: A Real?World Example

A recent survey of 1,200 borrowers revealed that:

| Borrower Score | Average APR (%) | Typical Loan Amount (£) |

|---|---|---|

| 300–579 | 18.4 | 2,500 |

| 580–679 | 13.7 | 5,000 |

| 680+ | 8.9 | 10,000 |

This data underscores that while low?score borrowers can secure loans, the cost is proportionally higher.

Collateralised Loans: Lower Rates, Higher Risk of Asset Loss

For those willing to pledge an asset—typically a vehicle or property—lenders often offer more favourable terms. The collateral acts as security, reducing the lender’s exposure and allowing for lower APRs.

- Vehicle?Secured Loans: Must be less than ten years old, titled in the borrower’s name, and fully insured.

- Property?Secured Loans: Require a first lien on real estate; often only available to borrowers with strong equity positions.

While this route can bring rates down to the 10–15% bracket, it comes with the risk of asset forfeiture if repayments lapse.

How OneMain Financial Handles Collateral

OneMain Financial is a notable example. They allow borrowers to use cars as collateral, provided the vehicle meets their strict criteria. The company’s arizonaziploan.com partner offers similar services in Arizona, giving local residents access to competitively priced secured loans.

Pros of OneMain include:

- No pre?payment penalties.

- Same?day funding for approved applicants.

- Flexible repayment dates that can be aligned with paychecks.

Cons revolve around the potential loss of the vehicle and a higher origination fee, which can range from 1% to 10% depending on state regulations.

Fees: The Hidden Cost of Personal Loans

Beyond interest, borrowers must account for several fees that can inflate total repayment costs:

- Origination Fees: Ranging from £25 to £500, or a percentage of the loan amount.

- Late Payment Penalties: Often a flat fee or a percentage of the missed payment.

Administrative Fees: Some lenders charge up to 10% for paper copies of the agreement.

Transparency is key. Always read the fine print and ask the lender to itemise all fees before signing.

Comparing Fee Structures: Avant vs. Upstart

| Lender | Origination Fee | Late Payment Penalty |

|---|---|---|

| Avant | 0–10% | £25 or 5% of missed payment |

| Upstart | 0–8% | No late fee for first missed payment, then £50 thereafter |

These differences can mean the difference between a manageable debt load and an escalating financial burden.

Pre?Qualification: A Soft Credit Check to Gauge Eligibility

Many lenders offer pre?qualification tools that perform a soft credit check, giving borrowers a glimpse of potential rates without affecting their score. This feature is especially useful for low?score applicants who want to avoid hard inquiries.

- Avant’s Pre?Qualify: Provides an estimated rate and loan amount instantly.

- Upstart’s Soft Credit Tool: Shows a range of possible APRs based on your profile.

Using these tools can save time, reduce the risk of rejection, and help you compare offers side?by?side.

Strategic Tips for Low?Score Borrowers

- Maintain a Low Utilisation Ratio: Keep credit card balances below 30% of limits.

- Avoid New Hard Inquiries: Each hard pull can dip your score by a few points.

- Check for State?Specific Caps: Some states have stricter APR caps or fee limits.

- Consider Co?Signers: A co?signer with a stronger credit history can secure better terms.

These strategies, combined with a thorough review of lender offerings, empower borrowers to make informed decisions.

Regulatory Changes in 2026: What Lenders Must Do Now

The Financial Conduct Authority (FCA) introduced new guidelines aimed at protecting consumers with weak credit. Key points include:

- Transparent Fee Disclosure: All fees must be clearly listed before the contract is signed.

- No Misleading Rate Promises: Advertised rates cannot differ from actual APRs by more than 2%.

- Mandatory Repayment Flexibility: Borrowers can request a payment holiday for up to 30 days without penalty.

Lenders who fail to comply face hefty fines and potential licence revocation. For consumers, this translates into greater protection against hidden costs and unfair practices.

Impact on Low?Score Lending Markets

The new regulations have pushed lenders toward more responsible underwriting. As a result:

- Lenders are offering clearer loan terms, reducing the risk of “surprise” fees.

- Some high?rate products have been curtailed or rebranded to comply with caps.

- Borrowers report higher satisfaction rates due to improved transparency.

These shifts are a welcome development for anyone navigating the complex world of personal finance.

Choosing the Right Lender: A Checklist

Below is a quick reference guide to help you compare potential lenders:

| Feature | Avant | Upstart | OneMain Financial |

|---|---|---|---|

| Minimum Loan Amount (£) | 1,000 | 1,000 | 1,500 |

| Maximum APR (%)* | 25 | 22 | 30 |

| Origination Fee Range | 0–10% | 0–8% | 1–10% |

| No Pre?Payment Penalty | Yes | Yes | Yes |

| Collateral Option | No | No | Yes (vehicle) |

| Funding Speed | Next day | Instant pre?qualify, then next day | Same day for approved |

* APR caps vary by state and lender policy.

Final Thought: Empowerment Through Knowledge

Personal loans need not be a source of anxiety. By understanding how credit scores influence rates, recognising the importance of fee transparency, and staying abreast of regulatory updates, borrowers can secure the funds they require without falling into predatory traps.

Whether you choose an AI?driven platform like Avant or Upstart, or opt for a secured loan through OneMain Financial, remember that every decision carries long?term implications. Take your time, compare offers carefully, and never hesitate to ask questions before signing.

For residents of Arizona looking for competitively priced secured loans, consider exploring options available via arizonaziploan.com. Their streamlined application process can help you navigate the complexities of personal lending with confidence.

For further reading on how credit scores affect loan terms, visit the Consumer Financial Protection Bureau. And to stay updated on the latest lending regulations, check out the Financial Conduct Authority.

Posted on March 8th, 2026 by Anthony Levene